The treacherous final mile: why embedded inflation is harder to beat

Summary

Central banks in the U.K. and U.S. struggle to hit the 2% inflation target because price increases have become domestically entrenched (especially in the U.K. via wages), creating a risky dilemma: holding rates too high harms economic growth, but cutting too soon risks permanently high inflation.

Welcome to Capital markets: strategy and risk, a new series where our leaders and experts help you navigate the complexities of today's capital markets and make informed and strategic decisions.

A long fight against persistent inflation

After the post pandemic sharp rise, central banks have brought inflation somewhat under control through monetary policy tools. However, inflation does remain stubbornly above target in both the U..K and the U.S. In our recent semiannual market update webinar, Amol Dhargalkar, Chatham Financial’s Chairman, captured this difficulty, describing this last leg down in inflation as “a treacherous journey".

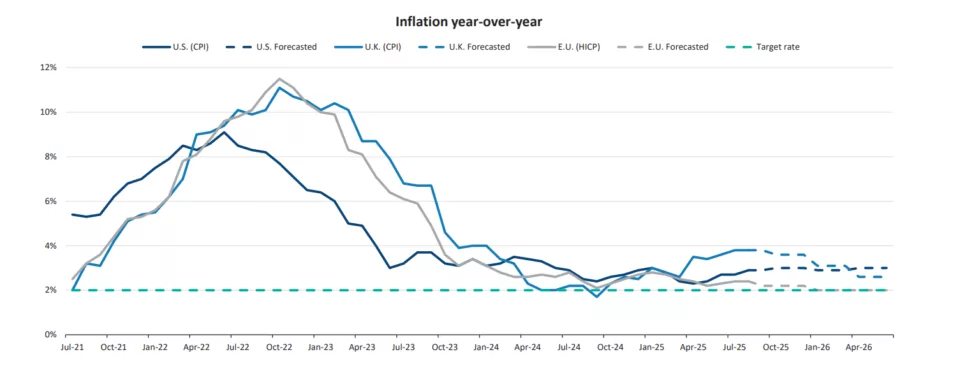

A tale of two inflation paths

While U.S. core inflation (as measured by PCE) is running slightly north of target, the inflation picture looks very different across Europe: the Eurozone is on track for its 2% target, while the U.K.’s higher, more entrenched domestic inflation is the greater concern. In particular, the wage growth levels have been concerning for the central bank.

Source: U.S. Bureau of Labor Statistics, Eurostat, ONS, and Bloomberg, revised September 23, 2025

From external shocks to embedded pressures

The inflation surge was primarily an external shock, driven by imported factors like energy prices following geopolitical events and the supply side constraints triggered by the lockdown response to the Covid pandemic. Some of the subsequent reduction came from the "change in the base effect" as these initial spikes rolled out of the 12-month measure.However, in the U.K., the inflation that remains is far more insidious. On the same webinar, Jackie Bowie, Chatham Financial’s Head of EMEA, explained that this last leg is proving difficult because the inflation is "much more embedded into the domestic economy, which makes it much harder to remove it". This domestic embedding is visible in the wage cycle and, notoriously, in food pricing in the U.K., where price inflation is a widespread concern for everyday consumers.

A delicate balance for policymakers

This is a significant predicament for policymakers. With inflation still near 4% against a 2% target in the U.K., Jackie noted that the Central Bank is in a "real tricky spot". The attempt to reach the target is subject to a two-fold risk. If policymakers hold current interest rates for too long, they risk impacting the growth of the economy. However, cutting too aggressively, they risk allowing inflation expectations to become permanently anchored above the target.

Given the levels of government debt there is a theory that there could be a ‘preference’ for slightly higher inflation as this could "inflate away" this sovereign debt pile. Investors do not take comfort in this idea, and central bank credibility could become an issue.

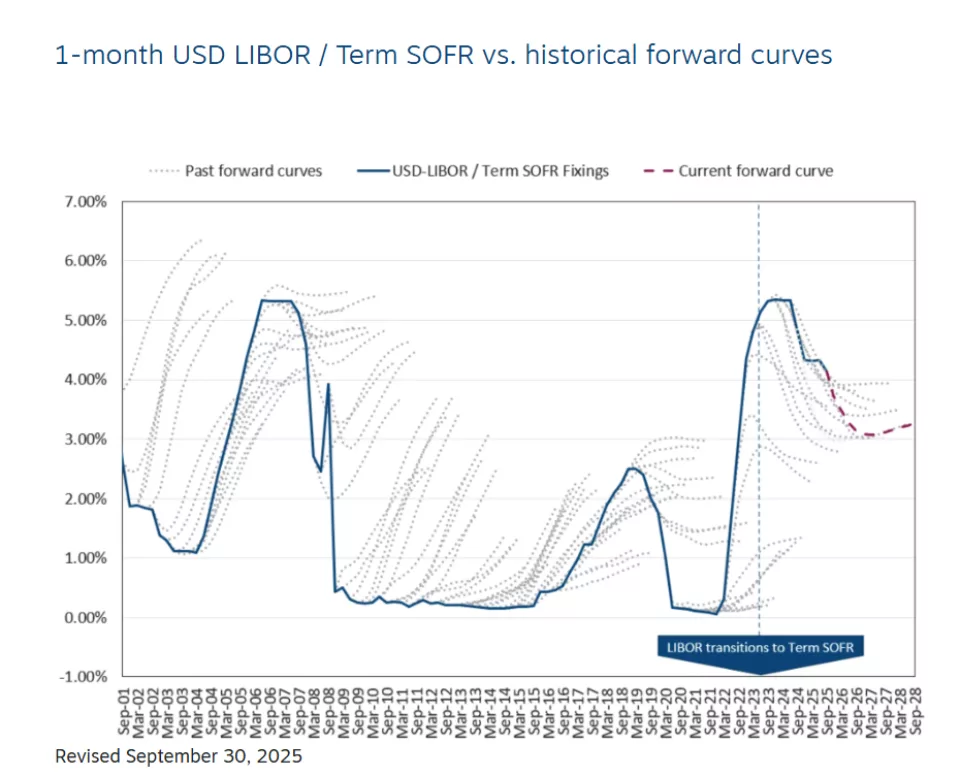

Market signals and implications

Bringing inflation back to target in both the U.S. and U.K. has proven far more complex than central bankers or markets initially anticipated. The persistence of price pressures, coupled with uneven economic data, has forced repeated reassessments of the policy path and created pronounced volatility in rate expectations. The “hairy” forward curves now reflect not just uncertainty about the timing and pace of cuts, but also questions over where equilibrium rates might ultimately settle.

Source: Chatham Financial, revised September 30, 2025

Navigating the final stretch

While the fight against inflation may be entering its final stages, it is unlikely to be a straight path. Central banks will need to balance credibility with flexibility, ensuring policy remains tight enough to finish the job but responsive enough to avoid unnecessary strain on growth. For investors and borrowers alike, this period calls for agility, close attention to policy signals, and readiness to recalibrate as new data reshapes the outlook.

Subscribe for more insights

Get the latest insights from Chatham delivered to your inbox weekly.

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

25-0113